View from the Top: Arcus Innovation Leaders Series. How business leaders use innovative approaches to shape their strategies. A message for CEOs on performance benchmarks, transformation of organizations and performance systems. An interview with Mr. Alan Depencier, Head, Marketing Services and Transformation at RBC.

Innovation in Financial Services: RBC Royal Bank

Mr. Depencier says it is critical to have the right people to champion projects and technology, supported by visible senior level sponsorship. The transformation of organizations usually occurs across several years whereas continuous improvement can potentially take place every quarter. The key driver of success will be the ability of an organization to structure its teams around these initiatives.

Read the Arcus Innovation Leaders Report

What does it take to innovate? Arcus Consulting Group has launched a major initiative to explore growth and innovation as key elements of corporate and business unit strategy. A majority of executives say it involves a pervasive corporate culture, deeper customer insight and a comprehensive strategy that will enable an organization to offer its customers important added value. They say such steps reduce costs, increase sales and achieve higher earnings. But how does one come up with new solutions, and can innovation really be part of a strategy plan? Arcus’ multi-industry survey of over 1,500 senior executives found that of all the challenges companies face in this area, the biggest challenge is finding ways to create a “culture of innovation

As Arcus research indicates, doing so means that you need to be surrounded by highly talented people. It also means finding a way to transmit your passion to them, so they will buy into your vision of the future, perform at the highest possible levels, and come up with innovative solutions to the challenges of achieving the vision. No surprise, then, that the topic of innovation has been gaining ground as CEOs seek to incorporate concepts like “a culture of innovation” into their assessments of a company’s long-term value.

An interview with Mr. Alan Depencier, Head, Marketing Services and Transformation at RBC.

Arcus: What is the biggest challenge companies face today in the area of innovation?

My experience indicates that the biggest challenge is in operationalizing innovation. Most organizations have lots of new ideas. But defining the process of validation of these new ideas is a significant opportunity. I would think it is also important to have a persuasive business case for each new idea. The business case needs to be based on the business benefits of the idea, its impact on consumers and proper validation of the ideas in research. The scale of our operations means we are in a position to accelerate the process.

Today, managers can’t just work on long term goals. This is especially true for middle managers. They have to deliver aggressive goals today. And then it’s possible to add a transformational project. The challenge has to do with finite resources. In addition, reorganization can be disruptive too. You have to bring new people on board if there are changes which can slow the innovation process.

Are there specific areas within organizations that drive innovation?

I think there are three areas: First, having the right people to champion projects and technology, supported by visible senior level sponsorship. Having the right people on a project is critical because we have found different outcomes from people managing similar projects.

Second, we are finding that all our work in the area of innovation has a technology component. It impacts most of our services and our systems. For example, if we are delivering a new product, our legacy systems may be a big barrier. One of the challenges is the cost and time for implementation of technology related projects. Due to the variable cycles of these initiatives, you need to have short and long term goals. For example, an organization may have a patch work of systems built over time. This could be a multi-year transformational project. The work around innovation may be limited until the transformation of the technology is completed.

“We are finding that all our work in the area of innovation has a technology component.”

The third area is senior level sponsorship. We find that innovation for ongoing initiatives happen naturally. These innovations evolve current strategies and do not require senior sponsorship. For example, you may have a current strategy around your value proposition or offering for a line of business. And you are continually trying to better communicate it with a promotion or advertising campaign. This is a process of continuous improvement. The next layer of transformation requires a whole new way to deal with innovation.

Does short-term and long-term innovation intersect?

Both need to happen at the same time. We have found that transformation usually occurs across several years. Whereas, continuous improvement can potentially take place every quarter. These two areas do cross paths at certain points. For example, we are working on our client contact rules. We are in a multi- channel environment. In the past, financial services companies had only branch and phone channels to communicate with customers. Today, we have branch, phone, internet, mobile and several others.

“We have made a commitment to look after the client’s best interests.”

We recently did an analysis and found that we have one billion contacts with our clients each year. That includes proactive contact with our clients. Some are low touch, like a financial statement. And others are high touch, like proactively contacting a client to offer a product that they may not be aware of. So client contact rules are a significant opportunity. We have different lines of business that are trying to grow their P&L. Hence, there may be a need to have a higher level of contact across business units with the same client.

The key here is communication channel management. We have made a commitment to look after the client’s best interests. We have one client who may need a select set of services. We need to identify the most relevant and timely communication channels that create value for the client and also have a positive impact for us.

How do you manage a multi-channel contact environment for each client?

It is a complex process because we have one client who is expecting us to talk about topics that are relevant to them. We also have new ideas, opportunities and products to talk to the client about. There are also the marketing and operations aspects. All these opportunities translate into communication opportunities. Yet, a client may want to talk to us just four times a year.

From a client perspective, that’s a significant transformation. We will contact our clients only when it is appropriate and relevant. This addresses our “Client’s First” positioning. We create client contact rules that deliver on that promise. We need to balance the client’s needs with their requirements for our products and services. We need to define the most appropriate and relevant channel. Some channels are not as intrusive- such as financial statements. While others may be higher touch ones that need to be planned carefully.

Has the approach of multi-channel contact management translated into tangible results?

One of our big advantages is how enabled we are in our marketing channels. Last year our organizations did a billion communications, broken into channels such as telemarketing, direct, branch, statements, ATM. Even within these vehicles we have inbound, outbound, inserts, direct mail, online, message centre, content, etc. Part of our client contact rules is to match our client’s current financial holdings with the right communications.

For example, it is possible that a client may be in the market for a mortgage but also reviews information about credit cards. Based on specific behavioural data, it may be possible to define the type of credit card that may be of interest to the client.

How do you manage these diverse channels?

We have evolved from mass campaigns to micro targeting. Client information needs trigger a marketing activity based on what the client has told us or certain behaviours of the client that would suggest a specific need or opportunity. Typically it is well received compared to mass communication. For example, if a client downloads an article about buying a first home. It’s possible that the client may be interested in relevant information related to homes.

At a later stage we may proactively reach out to the client to create awareness and engagement. It is much more targeted, timely and relevant. For us, the key questions to ask are: did it breakthrough, did it get linked to the brand, did it communicate the main message and did it persuade the consumer to take action. We are sophisticated with regard to measurement, especially with direct mail supported with traditional letters, statements and online measurements. The more challenging measurements relate to mass advertising.

“We have found that having a client first approach can result in a mini discovery.”

The marketing mix measurement model is unique for us because unlike, for example packaged goods, we have a database of our clients and can measure responses. We have a good view of the value chain. Most of our campaigns are multi channel, in branch, online, TV and radio. We can get a clear read on which medium has the most impact.

The key to success is marketing spend optimization. Someone said “50% of our spend is wasted, I don’t know which 50%”. But that’s not the case today. We have a good sense of the areas of marketing that are delivering superior results.

Financial services have a broad range of services. We have found that measurement in different media channels are at different levels of sophistication. Every category has its own response rate. For example, purchasing a mortgage is very different from purchasing a credit card. Even within insurance, you have home, auto and travel. In loans, you also have many different options. Our tracking program can analyse customer information to create clusters of clients who are reviewing options but have a considered and preferred set. We do that on a monthly basis across product lines.

How have you integrated the diverse media to optimize measurement tools?

We have integrated all our media such as direct, TV and online under one umbrella and one team. We also have a good understanding of purchase cycles. For example, a mortgage a purchase cycle may be longer than a credit card purchase cycle. We tended to silo our measurements. Marketers used to get frustrated when they received parts of the puzzle. We still need pulse reports but the information needs to be put together into one story at the end of a period. These are examples of continuous improvement.

The process of developing advertising is also going through continuous improvement especially in large organizations with many stakeholders. Unlike, Consumer packaged goods, where you tend to have silos in marketing, in our industry, product, distribution channels (branch online etc), pricing, marketing and promotions are managed by marketing. The four P’s are integrated to deliver superior results.

What complexities do teams face with multi-channel integration and management?

There are multi-channels that have an internal and external viewpoint for measurement and integration. A marketing manager has to determine what levers need to be pulled because you have a common client across products. Other marketing managers may be targeting the same client. That’s why client contact rules are so important. For example, if a client calls to check a balance, we will satisfy the initial need. We have found that having a client first approach can result in a mini discovery. It’s about getting our clients to talk to us about their needs. The challenge is in prioritization. There may be 25 products and services to talk about. We need to address the challenge of prioritizing the offering.

Are there specific challenges around senior level sponsorship?

Most organizations will agree that projects are unlikely to succeed without senior level sponsorship. There are multiple stakeholders. You need to enable marketing channels over time and integrate stakeholders in a linear value chain.

We find that the key is how you take an idea and whet it properly. It requires a high level analysis linked to business benefits. Can we really operationalize it inexpensively and quickly or is it a multi-year project? What is the risk?

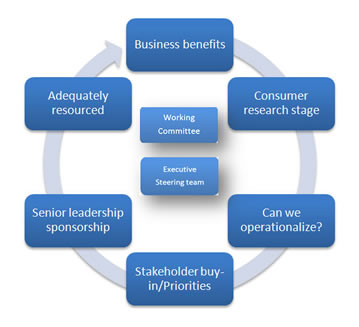

“The approach of identifying the best ideas is critical because it can ensure stakeholder buy-in.” How would you approach the process of operationalizing promising ideas?

There may be other projects in progress. How does this new project integrate with other projects?

After stakeholder buy-in, it’s important to determine if you have the right people leading the project with the support of cross functional groups. First, good relationships are an important part of delivering superior results and second, it’s important determine if the project is resourced adequately. Having someone work on it part-time is unlikely to deliver the same results as a full time resource. Third, other cross functional areas also need to commit time to the initiative. And fourth, you need an executive committee to be involved. You may have a working group that could include sales, product groups and channel managers. The team leaders of each representative in the working group would be part of the steering committee. It’s quite common to run into barriers every week. You need a monthly steering committee to manage these barriers.

How do you prioritize between new and existing initiatives?

First, it’s important to focus on existing ideas. The approach of identifying the best ideas is critical because it can ensure stakeholder buy-in. These existing ideas are not revolutionary. A lot of our partners have implemented them. These are unlikely to be true breakthrough innovations that will they differentiate us in the market place. But they are strong innovative ideas that will have an impact on our performance. These ideas can either impact our bottom line or our clients or both.

Second, we have found that resource allocations are always linked to potential time constraints. It may be more efficient to break down large marketing transformation projects into smaller phases and milestones. This will enable the team to celebrate successes throughout the transformation project. For example, our approach is to launch a new phase of a transformation project every quarter or every six months. A manager responsible for innovation usually leads the marketing transformation initiative. It is important for the steering committee should take ownership and should see it as their idea no matter where it originated.

Do you see differences in the approach on transformation projects in CPG and financial services?

In packaged goods, the scale is smaller and the 4 Ps are controlled in the marketing function. The 4Ps in banking are integrated at a senior level. In packaged goods, you are selling one products that may not affect other businesses. But in financial services, you may have one brand, one client and multiple products and services. The performance of one product can affect the entire line of business. Also in banking, the organization owns the distribution channel, where as in packaged goods, there are numerous external channels of distribution. Our processes require stakeholder buy-in and marketing of ideas throughout the organization. Packaged goods tend to have global centres of excellence, where local markets tap into long term innovation. But the focus is on local implementation of these ideas.

How do you approach risk management in context of innovation and change?

Our approach is to take proven ideas and roll them out. For example, we could rather invest ninety percent of our innovation resources in proven initiatives. Eight percent of the remaining resources could be allocated to external innovation that may not be done at RBC and the remaining two percent of resources may be allocated to initiatives that have probably not been done elsewhere. Our focus is on risk management and driving immediate and long term performance. It could be a linear process with each stage driving the innovation continuum.

“You need to look at how to innovate on an ongoing basis.”

We are fairly confident about the performance and ROI of the investments in proven initiatives. In other transformation areas, we have a high level of confidence we will see an ROI down the road but it will take time to test it and build it. Over time it may work for only some categories. And the two percent is much further down the paradigm of time to market. It’s a time related risk and ROI model. For example, ERCM is a big space with significant initiatives over the next five years. After one piece is completed, it moves into the 90% space. It’s with a view of what the future looks like and with a set plan of where we are going.

Another analogy may be the structure of investment portfolios. You may have blue chips, small caps and venture capital opportunities with varying risk and return profiles. Innovation is beneficial if it isn’t disruptive for the organization. It’s quite likely that Capital Markets have more radical innovations that the Financial services sector.

Does innovation in marketing have different challenges?

Innovation in marketing is a bigger challenge. Marketing has the pressure to differentiate products without dramatically different product features. But most products are not unique or innovative. Mature categories tend to have more innovation in the marketing space while merging categories tend to see more innovation in the product space.

You need to look at how to innovate on an ongoing basis. An innovation continuum could potentially include three distinct phases aligned with priorities for the next 12 months, 3 years and a long term transformation initiative for bigger ideas. The key driver will be to organize teams around these phases.

Please contact Merril Mascarenhas, Managing Partner at Arcus Consulting Group at (416) 710-2727 or by email for more information and to provide your feedback to RBC and Arcus.